Life insurance and life insurance policies are often seen as necessary steps in securing financial stability for loved ones after a death. Yet, for many Black Americans, life insurance policies were once considered primarily for covering funeral costs, offering only minimal coverage. This perception has been shifting, especially in recent years. Black Americans are now purchasing more life insurance and life insurance policies than ever before—not just as a safety net for burial expenses but also as tools to protect their families, build wealth, and fund future education. Understanding these evolving trends is crucial, as life insurance and its policies play a significant role in long-term financial planning.

A key shift is that more Black Americans are recognising the broader benefits of life insurance. No longer just a simple solution for funeral costs, life insurance is now seen as a financial tool for growth, stability, and protection. This change, largely driven by education and the need for generational wealth, is reflected in both survey statistics and expert advice.

In this article, we’ll explore 13 key facts about Black Americans buying more life insurance policies. These facts show how attitudes are changing and why life insurance is becoming a vital part of financial planning in Black communities. We’ll also discuss the impact of recent events like the COVID-19 pandemic, and how it brought the importance of life insurance into focus.

1. Covid-19 Boosted Life Insurance Sales Among Black Americans

The Covid-19 pandemic had a significant impact on many aspects of life, and one of the most notable changes was the surge in life insurance purchases, especially among Black Americans. Before the pandemic, life insurance might not have been a top priority for many. However, as Covid-19 spread rapidly and caused devastating losses, more Black Americans began to realise the importance of having life insurance in place.

How Covid-19 Affected Life Insurance Purchases

The pandemic highlighted the fragility of life, and it made people more aware of their own mortality. Black Americans, in particular, were hit hard by the virus. They experienced higher infection rates, hospitalizations, and death tolls compared to other racial groups. This led many to reconsider their financial preparedness for the unexpected.

In fact, research from financial institutions like LIMRA (Life Insurance Marketing and Research Association) found that nearly a third of all consumers reported they were more likely to buy life insurance because of the pandemic. However, this number was higher among Black Americans, who were facing disproportionate health risks. This sharp increase in life insurance interest was not only driven by concern for immediate family security but also for the long-term financial protection of loved ones.

A Key Factor in the Decision: The Realisation of Mortality

For many, the pandemic served as a wake-up call. The constant news of illness and death caused people to reflect on their own lives and families. As a result, life insurance became a practical and necessary financial product for those who had never considered it before.

As Alison Salka, a senior vice president at LIMRA, mentioned, the pandemic forced many to confront the idea of mortality in a way that was previously avoided. “People started thinking about the worst-case scenario, which made life insurance an essential part of their financial plan,” she said. This shift in mindset helped bring life insurance to the forefront of financial decision-making for Black families.

Key Factors That Drove the Increase in Life Insurance Sales

Several factors contributed to the higher rates of life insurance purchases among Black Americans during the pandemic:

- Increased mortality rates: Black Americans faced some of the highest death rates from Covid-19, which raised awareness of the need for financial protection in case of an untimely death.

- Health disparities: Limited access to healthcare and higher rates of underlying health conditions meant that the Black community was particularly vulnerable. This sparked a need to secure family financial stability in case the worst happened.

- Fear of economic hardship: The economic challenges brought about by the pandemic, including job losses and financial instability, led to more people wanting to ensure their family’s financial security, even in the face of uncertainty.

Expert Advice: Why Life Insurance Matters More Than Ever

From my years of experience in the industry, I can say that the most critical factor in choosing life insurance is recognising that it’s not just about replacing income after death. Life insurance serves as a tool for financial stability and peace of mind. It’s especially important for Black families, who, due to systemic inequalities, often face greater financial strain compared to other groups.

During the pandemic, many realised the importance of securing their loved ones’ future without leaving them burdened by unexpected expenses. If you haven’t yet considered life insurance, now is the time to think about it seriously.

Here are a few important points to consider when purchasing life insurance:

- Understand the types of policies: There are different types of life insurance, such as term life, whole life, and universal life. Each comes with its own benefits depending on your financial goals and family needs.

- Don’t overlook the coverage amount: Make sure the policy covers not just funeral expenses, but also other financial burdens like debts, mortgage payments, and education costs for children.

- Get advice from a professional: Consulting with an insurance agent who understands your unique financial situation can help you choose the right coverage.

The Future of Life Insurance in Black Communities

As the Black community continues to face challenges, particularly in terms of wealth disparity and economic security, life insurance will play an increasingly important role. The pandemic served as a pivotal moment for many Black families to shift from just surviving to planning for the future.

Ultimately, life insurance is not only a financial safety net; it can also be a way to build generational wealth. By having the proper coverage in place, you’re ensuring that future generations won’t inherit financial burdens, but instead, they’ll have the means to thrive.

2. Growing Recognition of Life Insurance Value

In recent years, more Black Americans have started to realise the value of life insurance beyond its traditional role of covering funeral costs. Historically, many viewed life insurance as something that only helped with burial expenses. However, today, more individuals are recognising how it can serve as a financial safety net, protect their loved ones, and even help build long-term wealth.

Why Life Insurance is Valuable Beyond Burial Costs

For years, life insurance was sold primarily as a product to cover funeral expenses. Unfortunately, this narrow view led to many people buying small, low-value policies that didn’t provide much benefit. Today, however, life insurance is seen as an essential part of financial planning, especially for families looking to protect their future.

Many Black Americans now understand that life insurance can help in multiple ways. It’s no longer just about paying for a funeral; it can also be used to:

- Pay off debts: Life insurance can help clear any outstanding debts or bills that might burden a family after the policyholder’s death.

- Provide for living expenses: It can replace the income lost when the main earner passes away, helping to keep the family financially secure.

- Fund education: Proceeds from life insurance policies can be used to pay for children’s education, providing a chance for future generations to succeed.

The Role of Education in This Shift

The change in mindset regarding life insurance is largely due to increased financial education. For years, Black communities were often misinformed or undereducated about the full benefits of life insurance. Many agents and companies are now working to change that by offering clearer information and helping people understand how life insurance fits into long-term financial planning.

A key part of this shift is the growing number of financial advisors who are focusing on educating people about life insurance as a tool for wealth building. Erwin McGowan, a State Farm insurance agent, explains, “Our people don’t know enough or don’t see the value of life insurance. That’s why it’s important to help those who need it most.” This message is resonating strongly with many families who now see life insurance as a way to protect their financial future.

The Broader Impact on Black Families

For many Black Americans, life insurance is seen not just as a safety net, but as a way to help build and preserve wealth for future generations. As Alison Salka from LIMRA points out, “Life insurance is a tool to protect your family if something happens to the primary earner.”

In fact, many families are now using life insurance policies to:

- Pass on generational wealth: Life insurance can create a financial legacy, helping to transfer assets and wealth to the next generation.

- Enhance financial stability: By ensuring that loved ones are not left struggling after the death of a breadwinner, life insurance offers long-term stability.

Personal Story: A Shift in Thinking

I’ve seen this shift firsthand in my work. A few years ago, many of my clients only sought the minimum coverage, mainly for funeral expenses. Today, I regularly see families looking for policies that can support them in other ways. One client, a single mother of two, recently shared how she bought a larger life insurance policy not only to cover her burial but also to ensure that her children could attend college without the added stress of financial burdens. This is the kind of change we’re seeing across the board.

The growing recognition of life insurance value among Black Americans represents a positive shift towards greater financial literacy and security. As people become more aware of its broader benefits, life insurance is transforming from a simple safety net into an essential financial tool. Families are now better equipped to protect their loved ones, build wealth, and leave a lasting legacy.

3. Life Insurance as a Tool for Funeral Coverage

For many Black Americans, life insurance has long been seen primarily as a way to cover funeral costs. This tradition dates back to the time when life insurance was often marketed as burial insurance, with minimal coverage that focused mainly on paying for funeral expenses. In fact, it wasn’t unusual for people to purchase small, inexpensive policies that would provide just enough money to cover the basic costs of burial, such as a coffin and cemetery plot.

However, there has been a noticeable shift in how life insurance is viewed within the Black community. The pandemic, in particular, brought death and mortality to the forefront of people’s minds, making many realise the importance of planning for such events. Now, many Black families are opting for policies that offer more than just funeral coverage. They are seeking life insurance that can help them address a variety of financial needs, beyond simply paying for a funeral.

Historical Context: Funeral Insurance vs. Comprehensive Life Coverage

Historically, life insurance companies targeted Black Americans with funeral insurance policies, promising them peace of mind in case of death. Unfortunately, these policies often had small payout amounts that didn’t truly address the needs of families. For example, some policies might only offer a few thousand pounds, which would barely cover the cost of a simple funeral, let alone help the family after the death of a loved one.

In many cases, door-to-door salespeople selling these policies weren’t always transparent about the full scope of coverage or the benefits of larger policies. This lack of education left many people with policies that didn’t offer long-term financial security.

Modern Shift: Life Insurance for More Than Funeral Costs

Today, Black Americans are beginning to see life insurance in a broader context. While many still use it to cover funeral costs, there is a growing understanding that life insurance can also provide financial support for surviving family members, pay off debts, and even leave behind an inheritance.

Here are a few reasons why life insurance is no longer just about funeral expenses:

- Protecting loved ones: Beyond paying for burial costs, life insurance can provide money to cover living expenses for family members left behind.

- Paying off debts: Many Black Americans are choosing policies that help clear existing debts, such as mortgages or car loans, so their families don’t face financial hardship.

- Building wealth: Some life insurance policies, like whole life or universal life, come with a cash value component, allowing policyholders to accumulate wealth over time.

The shift from basic funeral coverage to policies that provide financial security for the future is a positive trend. It reflects a broader understanding of life insurance as a tool for long-term financial planning, not just as a solution for covering end-of-life expenses.

Real-Life Example: A Growing Need for Education

As an expert in the industry, I’ve seen firsthand how important it is to educate people, especially in underserved communities, about the benefits of comprehensive life insurance. I remember working with a family where the mother had a small burial policy. Unfortunately, when she passed, the family realised that the policy didn’t cover all the expenses. Her children were left to manage the costs, which caused significant financial strain.

Since then, the family has worked with me to upgrade their coverage. They now have a policy that not only covers funeral expenses but also protects their home, and offers a safety net for their children’s education. This is a prime example of how life insurance can serve as a tool for financial protection, not just an end-of-life expense.

Key Points to Consider About Life Insurance for Funeral Coverage:

- Funeral insurance is the traditional view but is limited in scope.

- Comprehensive life insurance offers greater security by covering a variety of needs, including debts and future living expenses.

- Cash value policies can be a smart choice, offering a safety net while also growing over time.

- Education on the benefits of life insurance is crucial to helping families make better financial decisions.

By thinking of life insurance as a comprehensive financial tool, families can build a stronger foundation for the future. It’s no longer just about paying for the funeral—it’s about ensuring that loved ones are taken care of, no matter what.

4. Life Insurance as Family Protection

Life insurance is a crucial tool when it comes to protecting your family’s future. It’s about securing financial stability for your loved ones if something unexpected happens. If the main breadwinner of a household passes away, the surviving family members can face serious financial hardship. This is where life insurance steps in – providing them with the support they need to cope with loss while managing bills, living expenses, and future goals.

Why Is Family Protection Important?

When you purchase life insurance, you’re not just thinking about yourself; you’re planning for the future of those you care about most. Without life insurance, the sudden loss of a family member can put immense stress on the remaining family members, leading to a potential struggle to pay for day-to-day costs.

Having the right life insurance policy can help reduce this financial burden. This is because life insurance provides a lump sum of money upon the death of the insured, which can be used for a wide range of needs. Here’s why family protection through life insurance matters:

- Paying for everyday living costs: This can include rent or mortgage, groceries, utilities, and transportation.

- Covering education fees: If you have children, life insurance can ensure their education remains uninterrupted, even if you’re no longer around.

- Managing outstanding debts: Any loans or credit card debt that might otherwise become overwhelming for your family can be taken care of.

How Does Life Insurance Protect Your Family?

The key to understanding how life insurance protects your family is by knowing how the funds are used. The money provided by the policy can help to pay off debts, and most importantly, it can replace lost income, which is critical if the person who passed away was the primary earner in the family.

Here’s an example of how life insurance can provide family protection:

Let’s say a father passes away unexpectedly. If he had life insurance, the payout could cover the mortgage, car payments, and school fees for his children. Without it, the family might struggle to keep up with these expenses, leading to stress, anxiety, and financial instability.

In this way, life insurance offers a safety net, allowing the surviving family members to continue living their lives with fewer financial worries.

Types of Life Insurance for Family Protection

There are different types of life insurance, and each can serve a specific role in family protection. Here are the main options to consider:

- Term Life Insurance: This policy covers a set period, such as 10, 20, or 30 years. It’s an affordable option for families looking for basic protection for a specific time frame (e.g., until the children are grown or the mortgage is paid off).

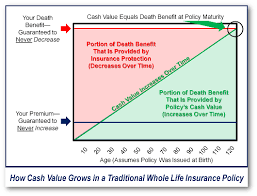

- Whole Life Insurance: A whole life policy offers lifetime coverage, meaning it doesn’t expire. It also builds cash value, which can be used for future financial needs.

- Universal Life Insurance: This type of policy provides flexible premiums and death benefits. It can also accumulate cash value over time, like whole life insurance.

Expert Advice: The Right Policy for Family Protection

As an expert in the auto insurance field, I’ve also seen the direct benefits of securing the right life insurance policy. One thing I’ve learned over the years is that underestimating the amount of coverage you need can leave your family vulnerable. Many families opt for policies that are too small, thinking that life insurance is a “one-size-fits-all” solution.

It’s essential to assess your family’s needs carefully and choose a policy that provides enough coverage. A good starting point is to consider factors such as:

- Your family’s monthly expenses

- Existing debts (e.g., mortgage, car loans, credit card debts)

- Your children’s education costs

- Future goals and retirement planning for your spouse

Taking time to get the right amount of coverage can make all the difference in ensuring your loved ones don’t face financial hardship after you’re gone.

How to Make Life Insurance Part of Your Financial Plan

Including life insurance as part of your overall financial plan is a smart way to guarantee that your family is protected, no matter what. However, it’s also important to stay informed and keep your policy updated as your life changes. For example, when you get married, have children, or buy a house, it’s a good idea to review your life insurance needs.

An important tip I often share with clients is to shop around and compare policies from different insurers. Rates can vary, and it’s essential to find the right policy for your budget without sacrificing coverage.

5. Transmitting Wealth through Life Insurance

Life insurance is not just about protecting your family in case something happens to you. It can also be a powerful tool for passing on wealth to future generations. For many years, Black Americans faced barriers to building wealth, partly because of systemic issues such as lower access to life insurance. However, that is changing as more people recognise that life insurance can be a means of leaving behind a financial legacy. In this section, we will explore how life insurance is increasingly seen as a way to transfer wealth and build a lasting financial foundation for descendants.

Why Life Insurance Matters for Building Wealth

Life insurance provides more than just a death benefit. It can act as a way to ensure that your family is financially secure after you are gone. While many people view life insurance primarily as a way to cover funeral costs, Black Americans, in particular, are increasingly using it as a means to leave an inheritance or fund other important expenses. This shift is important because it changes the narrative from life insurance as an emergency tool to a proactive wealth-building asset.

According to the New York Life study, 37% of Black Americans said they intend to use life insurance as a way to leave a legacy. This figure shows that more people are thinking beyond the immediate and focusing on creating long-term financial stability for their loved ones.

How Life Insurance Helps Close the Wealth Gap

The wealth gap between Black and White families has been well documented, with Black families having a net worth far lower than their White counterparts. In fact, Black families’ net worth is less than 15% of that of White families. Life insurance offers a way to bridge this gap. By providing a death benefit that can be passed on, life insurance allows Black families to leave behind wealth that might otherwise be unattainable.

Using life insurance as a wealth-building tool is not a new concept. In many cases, people use life insurance to pass on money for things like:

- Education: Life insurance proceeds can be used to fund a child’s education, reducing the financial burden of tuition.

- Homeownership: It can help family members make down payments on homes, creating long-term financial stability.

- Business Ownership: Some people use life insurance to pass on funds that can help family members start or expand a business.

These are all ways that life insurance can be part of a larger strategy for financial independence.

Expert Insight: The Value of Life Insurance in Wealth Transfer

As someone who has worked in the financial services industry, I’ve seen firsthand how life insurance policies can be used to pass on assets. It’s important to understand that life insurance is not just about having a policy for the sake of having one. It is about thinking ahead and considering how the death benefit can serve your family for generations.

I remember working with a family where the parents had purchased life insurance with the express purpose of funding their children’s higher education. When the time came for the family to collect the policy benefits, the children were able to attend college without the burden of student loans, setting them up for a more financially secure future.

By taking a strategic approach to life insurance, families can set up inheritance plans and ensure that their financial legacy is passed on in a meaningful way.

How to Use Life Insurance as an Investment Tool

One of the ways life insurance is used for wealth transfer is through permanent life insurance, such as whole life or universal life policies. These policies don’t just offer a death benefit; they also accumulate cash value over time. This cash value grows on a tax-deferred basis and can be borrowed against or withdrawn during the policyholder’s lifetime.

The ability to accumulate cash value makes permanent life insurance a valuable investment tool. It’s not just a policy that pays out after death; it’s also a way to build assets that can be used during your lifetime.

Here are a few things to keep in mind when considering life insurance for wealth transfer:

- Policy type: Permanent life insurance offers the best opportunity for wealth building through cash value accumulation.

- Death benefit: The death benefit can be passed on tax-free to your beneficiaries, which can make it an attractive option for legacy planning.

- Loans and withdrawals: The cash value can be used to cover urgent expenses, like medical bills, or be reinvested to grow your wealth.

By using life insurance in this way, families can turn a simple policy into a long-term asset that benefits generations to come.

Key Takeaways

- Life insurance is increasingly viewed as a wealth-building tool among Black Americans, helping to close the wealth gap and pass on assets.

- Permanent life insurance policies (such as whole life) accumulate cash value, offering both a death benefit and an investment option for policyholders.

- The death benefit can be used for a variety of purposes, including funding education, buying a home, or starting a business.

- Life insurance provides an opportunity for generational wealth that can last long after you’re gone.

Transmitting wealth through life insurance is an essential part of financial planning for Black Americans, as it allows individuals to leave behind more than just memories. Whether it’s to fund a child’s education or to create a nest egg for future generations, life insurance plays a critical role in securing the financial future of your family. As awareness of these benefits continues to grow, more families will use life insurance not only for protection but as a strategic asset for wealth-building.

Life Insurance as Family Protection

Life insurance is a crucial tool when it comes to protecting your family’s future. It’s about securing financial stability for your loved ones if something unexpected happens. If the main breadwinner of a household passes away, the surviving family members can face serious financial hardship. This is where life insurance steps in – providing them with the support they need to cope with loss while managing bills, living expenses, and future goals.

Why Is Family Protection Important?

When you purchase life insurance, you’re not just thinking about yourself; you’re planning for the future of those you care about most. Without life insurance, the sudden loss of a family member can put immense stress on the remaining family members, leading to a potential struggle to pay for day-to-day costs.

Having the right life insurance policy can help reduce this financial burden. This is because life insurance provides a lump sum of money upon the death of the insured, which can be used for a wide range of needs. Here’s why family protection through life insurance matters:

- Paying for everyday living costs: This can include rent or mortgage, groceries, utilities, and transportation.

- Covering education fees: If you have children, life insurance can ensure their education remains uninterrupted, even if you’re no longer around.

- Managing outstanding debts: Any loans or credit card debt that might otherwise become overwhelming for your family can be taken care of.

How Does Life Insurance Protect Your Family?

The key to understanding how life insurance protects your family is by knowing how the funds are used. The money provided by the policy can help to pay off debts, and most importantly, it can replace lost income, which is critical if the person who passed away was the primary earner in the family.

Here’s an example of how life insurance can provide family protection:

Let’s say a father passes away unexpectedly. If he had life insurance, the payout could cover the mortgage, car payments, and school fees for his children. Without it, the family might struggle to keep up with these expenses, leading to stress, anxiety, and financial instability.

In this way, life insurance offers a safety net, allowing the surviving family members to continue living their lives with fewer financial worries.

Types of Life Insurance for Family Protection

There are different types of life insurance, and each can serve a specific role in family protection. Here are the main options to consider:

- Term Life Insurance: This policy covers a set period, such as 10, 20, or 30 years. It’s an affordable option for families looking for basic protection for a specific time frame (e.g., until the children are grown or the mortgage is paid off).

- Whole Life Insurance: A whole life policy offers lifetime coverage, meaning it doesn’t expire. It also builds cash value, which can be used for future financial needs.

- Universal Life Insurance: This type of policy provides flexible premiums and death benefits. It can also accumulate cash value over time, like whole life insurance.

Expert Advice: The Right Policy for Family Protection

As an expert in the auto insurance field, I’ve also seen the direct benefits of securing the right life insurance policy. One thing I’ve learned over the years is that underestimating the amount of coverage you need can leave your family vulnerable. Many families opt for policies that are too small, thinking that life insurance is a “one-size-fits-all” solution.

It’s essential to assess your family’s needs carefully and choose a policy that provides enough coverage. A good starting point is to consider factors such as:

- Your family’s monthly expenses

- Existing debts (e.g., mortgage, car loans, credit card debts)

- Your children’s education costs

- Future goals and retirement planning for your spouse

Taking time to get the right amount of coverage can make all the difference in ensuring your loved ones don’t face financial hardship after you’re gone.

How to Make Life Insurance Part of Your Financial Plan

Including life insurance as part of your overall financial plan is a smart way to guarantee that your family is protected, no matter what. However, it’s also important to stay informed and keep your policy updated as your life changes. For example, when you get married, have children, or buy a house, it’s a good idea to review your life insurance needs.

An important tip I often share with clients is to shop around and compare policies from different insurers. Rates can vary, and it’s essential to find the right policy for your budget without sacrificing coverage.

Key Takeaways:

- Life insurance is essential for ensuring your family’s financial stability if the worst were to happen.

- It can cover daily living costs, pay off debts, and ensure your children’s future education is funded.

- Different types of life insurance policies, such as term, whole, and universal, offer various benefits, so it’s important to choose the one that fits your needs.

- Regularly reviewing and updating your life insurance coverage ensures that your policy keeps pace with your family’s changing circumstances.

6. Life Insurance as a Financial Goal

For many Black Americans, life insurance has evolved beyond being just a basic safety net into a key part of their overall financial planning. Life insurance as a financial goal is now seen as a way to secure not just protection, but also long-term stability for their families. This shift in thinking has been important for closing the financial gaps that have historically affected Black communities.

Why is Life Insurance Seen as a Financial Goal?

Life insurance isn’t just about leaving behind a death benefit. It can be used as a way to achieve important financial milestones, such as saving for retirement, funding a child’s education, or even starting a small business. The idea of life insurance as a financial goal means Black families are now viewing it as a tool to build wealth, not just cover burial expenses. This approach helps families work towards bigger financial dreams.

The New Mindset: Proactive Financial Planning

Recent studies show that 80% of Black Americans now rank life insurance as one of their top financial goals. This is much higher compared to the general population, where only 63% of adults feel the same. For Black families, the desire to protect their loved ones and create a legacy has pushed life insurance to the forefront of their financial planning.

Personal Story: A Step Towards Financial Security

I’ve worked with many Black families over the years, and I can personally attest to the change in mindset. Many of my clients initially thought of life insurance only as a way to cover final expenses. But after discussing their financial goals—whether it was sending their children to college or saving for retirement—they started seeing how life insurance could serve as an essential tool in achieving those goals. This shift has been incredibly empowering for them, and it’s a trend that I believe will continue to grow in importance.

Benefits of Viewing Life Insurance as a Financial Goal

When life insurance is considered a financial goal, it brings many advantages to Black families:

- Wealth Accumulation: Some life insurance policies, like whole life or universal life, build cash value over time. This cash value can be used to support long-term financial goals, such as funding a child’s education or expanding a family business.

- Financial Protection: It ensures that family members are financially secure if the breadwinner passes away unexpectedly. This can help cover living expenses and prevent financial hardship.

- Tax Advantages: Certain life insurance policies have tax-deferred growth, meaning they can accumulate value without being taxed until the funds are withdrawn.

Why More Black Americans are Embracing Life Insurance as a Financial Goal

This change is driven by a broader understanding of personal finance within the Black community. African Americans are increasingly turning to trusted advisors to help them make informed decisions. The goal is to break the cycle of underinsurance and begin planning for the future, instead of just reacting to the present.

Moreover, many people are now more aware of the racial wealth gap. The median net worth of Black households is significantly lower than that of White households. As a result, Black Americans are taking more steps to secure their financial future by using life insurance as an additional asset to bridge this gap.

How to Use Life Insurance to Achieve Financial Goals

To make life insurance work as a financial tool, it’s important to choose the right policy and understand how it fits into the broader financial picture. Here are some ways it can be used:

- Cover Educational Costs: Many families use life insurance to set aside funds for their children’s college education. The policy’s cash value can grow over time, providing a source of funds for tuition or other educational expenses.

- Supplement Retirement Plans: Policies like whole life or universal life insurance can be used to supplement traditional retirement accounts, such as 401(k)s or IRAs. They provide an additional layer of security, especially as they accumulate cash value.

- Building Wealth: Some families use life insurance as an investment tool. By choosing policies that build cash value, the family can tap into this savings if needed for a business venture, a down payment on a home, or to cover large expenses.

- Leaving a Legacy: For many Black families, leaving a financial legacy for future generations is a top priority. Life insurance can help pass on wealth to children or grandchildren, providing them with financial stability.

Conclusion: Taking Control of Financial Futures with Life Insurance

Life insurance is no longer just a tool for covering funeral costs; it is now a part of the bigger picture of financial planning. By viewing life insurance as a financial goal, Black Americans are actively working to close the wealth gap, provide for their families, and build a more secure future. As more people become aware of the potential benefits of life insurance, we can expect this shift in mindset to continue growing, benefiting families and communities for generations to come.

By choosing the right policy and viewing life insurance as a way to achieve financial goals, families can build wealth and ensure their loved ones are financially protected, no matter what the future holds.

7. Financing Education Through Life Insurance: A Key to Securing Your Family’s Future

Life insurance is often thought of as a safety net in case of death, but it can also be a powerful tool for building a better future, especially when it comes to education. Many people are starting to see how life insurance can help fund their children’s education, creating opportunities for the next generation that they might not have had otherwise. This is an important shift in how Black Americans are viewing life insurance, moving from just covering funeral expenses to using it as a way to build long-term wealth for their families.

How Life Insurance Can Help Pay for Education

Life insurance policies, particularly permanent ones like whole life or universal life, often have a cash value component. This means that, over time, your policy grows in value. When the policyholder passes away, the death benefit is paid out to their beneficiaries. But there’s more to it than just the death benefit. The cash value can be accessed during the policyholder’s lifetime, and it can be used for things like paying for college tuition or other educational expenses.

- Cash Value Accumulation: Permanent life insurance policies accumulate cash value over time. This is a great way to set aside money for future educational costs.

- Loans Against the Policy: If you need funds sooner, you can take out a loan against the cash value of the policy. These loans typically have low-interest rates and can be paid back on your terms.

- Tax Advantages: The money accumulated in the policy often grows tax-deferred, which means you don’t have to pay taxes on the growth until you withdraw it.

For many Black families, the idea of financing a child’s education can seem like an overwhelming challenge. College tuition has risen sharply over the years, and the average family struggles to keep up. Life insurance can provide a cushion that makes it easier to afford education without falling into debt.

Real-World Example: Using Life Insurance for Education

Let me share a personal example to illustrate the impact life insurance can have. I once worked with a family who had taken out a whole life insurance policy when their child was born. The parents didn’t have a lot of money at the time, but they understood that this small investment would grow over the years. By the time their child was ready for college, they were able to access the policy’s cash value to help cover tuition fees. This wasn’t a large sum of money, but it was enough to take the pressure off student loans and reduce the financial burden on their family. They ended up saving more in the long run because they had used life insurance as a savings tool.

The Advantages of Using Life Insurance for Education

- No Need for Student Loans: Life insurance provides a way to fund education without relying on expensive student loans.

- Less Financial Strain: It can help ease the financial strain of tuition fees, textbooks, and other school-related costs.

- Generational Impact: This strategy can be passed down from one generation to the next, helping multiple children with their education. In the long run, this can significantly help break the cycle of financial struggle.

How Black Americans are Shifting Their View of Life Insurance

Historically, Black Americans have often viewed life insurance primarily as a way to cover funeral expenses. However, the shift towards using life insurance as a tool for education funding is a promising change. According to the New York Life study, 68% of Black Americans surveyed said they planned to use their life insurance proceeds to pay for a child’s college education.

This shift is crucial because it represents a change in mindset. Instead of seeing life insurance as a mere necessity for death-related expenses, Black families are now understanding its value in securing their children’s future and helping them achieve financial goals. Education is a critical factor in closing the wealth gap, and life insurance can play an important role in making that a reality.

Benefits of Life Insurance in Financing Education

- Guaranteed Money: Life insurance ensures that your children will have the funds needed for their education, no matter what happens in the future.

- Less Stress for Parents: Knowing that there is money set aside for educational costs gives parents peace of mind.

- No Restrictions: Unlike scholarships or grants, there are no restrictions on how life insurance proceeds can be spent. They can be used for tuition, books, housing, and even studying abroad.

8. Peace of Mind and Financial Security

Life insurance plays a significant role in offering peace of mind to families, particularly for Black Americans, who are increasingly recognising its value. It provides a sense of security knowing that, in the unfortunate event of a death, financial pressures won’t add to the emotional burden. This peace of mind is something that more people are starting to understand, as the conversation about life insurance grows stronger.

For many Black families, having life insurance means one less thing to worry about. Instead of wondering how bills will be paid or how the family will manage after the death of a loved one, the insurance policy steps in to provide the financial support needed to handle immediate expenses. This could include funeral costs, mortgage payments, or paying off debts that might otherwise fall on the shoulders of family members. With the right life insurance policy, the family can focus on grieving and healing rather than scrambling to make ends meet.

Why Peace of Mind Matters

- Immediate financial relief: Life insurance can cover funeral and medical expenses, which often come as a surprise when a loved one passes away. It allows the surviving family members to deal with loss without worrying about their finances.

- Ongoing security: In some cases, life insurance policies offer benefits that can continue to support a family long after the initial claim. For instance, monthly payouts can help cover regular bills such as utilities, rent, or even future education costs for children.

This kind of financial backup is crucial, especially in Black communities where generational wealth gaps often create financial stress. Life insurance is one of the few tools that can help fill in these gaps, helping families stay afloat during tough times.

A Personal Example

As an expert with years of experience in the insurance field, I’ve seen firsthand how crucial life insurance can be. A long-time customer of mine, Mr. Jones, had a modest policy just to cover funeral costs when he signed up. A few years later, when he passed away unexpectedly, his family not only had enough to cover the funeral but also to help his children pay for their education. Mr. Jones had realised the importance of having a life insurance policy that provided more than just funeral costs. His foresight and the peace of mind it gave his family are a perfect example of why understanding the full value of life insurance is so important.

What Life Insurance Offers in Terms of Peace of Mind

- Funeral Expenses Covered: At the very least, life insurance can ensure that burial costs are taken care of. Without life insurance, these expenses often fall on family members at a time when they’re least prepared to handle them. Life insurance eliminates this worry.

- Debt Management: Many people pass on debts, like credit card bills or loans, which can burden their families. Life insurance can pay off these debts, providing the surviving members with the breathing room they need to grieve without financial strain.

- Supporting Dependents: Parents, particularly, find life insurance useful for ensuring that their children are taken care of. From ensuring childcare expenses are covered to helping with schooling, life insurance helps secure their futures.

A Financial Safety Net for the Family

Having a life insurance policy is like putting a financial safety net in place. It’s something you set up today, not just for yourself, but for the future of your family. Whether it’s paying for education or securing a home, life insurance ensures that your loved ones can maintain a certain standard of living even if you’re no longer there to provide for them.

Some life insurance policies also offer cash value over time. This means that, besides the death benefit, the policy itself may accumulate savings that can be accessed by the policyholder during their lifetime. This can be a huge help in covering unexpected expenses, medical bills, or even funding a small business. It adds another layer of financial security, allowing you to use the policy as a tool for both short-term and long-term planning.

9. Saving Money with Life Insurance

Life insurance isn’t just about protecting your loved ones after you’re gone—it can also be a way to save money while you’re alive. Many people aren’t aware that certain types of life insurance can help build savings over time. If you’re looking for ways to save money for future needs, life insurance might just be one of the most overlooked options.

How Does Life Insurance Help You Save?

There are two main types of life insurance policies that can help you save money: whole life insurance and universal life insurance. These policies don’t just provide a death benefit—they also build up a cash value. The cash value grows over time and can be used for different things, such as covering unexpected expenses, funding a child’s education, or even adding to your retirement savings.

- Whole Life Insurance: This is a type of permanent life insurance that provides coverage for your entire life. In addition to the death benefit, a portion of your premium goes towards building the cash value. Over time, the cash value can grow and accumulate interest, providing you with a financial cushion.

- Universal Life Insurance: This is another type of permanent life insurance that offers more flexibility. You can adjust the premiums and death benefit amount as your life changes. The cash value also earns interest, though it may be subject to market fluctuations depending on the policy.

Both types of policies can help you save money in the long run, but there are key differences in how they work. It’s important to understand these differences before deciding which policy best suits your financial goals.

What Can You Do with the Cash Value?

The cash value in your life insurance policy can be used for various purposes. Here are some of the ways people use it to save and plan for the future:

- Pay for Emergency Expenses: If an unexpected bill or financial crisis arises, you can borrow against the cash value of your life insurance policy. This could be helpful if you don’t have an emergency fund or if you need to cover a large, unexpected cost.

- Supplement Retirement Savings: As the cash value grows, it can be used to supplement your retirement savings. The cash value can be withdrawn or borrowed against, providing you with an additional source of income in your later years.

- Pay Premiums: Some policies allow you to use the cash value to pay for your life insurance premiums. This can be a helpful option if you want to reduce your out-of-pocket expenses later in life.

- Cover Large Expenses: Life insurance can also be a way to save for significant future costs, like buying a house or paying for a child’s education. The accumulated cash value can be used to help fund these big milestones.

Advantages and Disadvantages of Using Life Insurance for Savings

There are some notable advantages to using life insurance as a savings tool, but there are also some drawbacks. It’s important to weigh both sides before making any decisions.

Advantages:

- Guaranteed Growth: With whole life insurance, your cash value grows at a guaranteed rate, providing a safe and predictable way to save money over time.

- Tax Benefits: The cash value in your life insurance policy grows tax-deferred, meaning you don’t pay taxes on the growth until you withdraw it. This can be an advantage if you’re looking to keep more of your savings.

- Flexible Access: Unlike other savings accounts, you can borrow against the cash value of your life insurance policy at any time. This can provide you with easy access to funds in case of emergency.

Disadvantages:

- Higher Premiums: Life insurance policies that build cash value tend to have higher premiums than term life insurance. This can make them less affordable for some people, especially those who are only looking for basic coverage.

- Slower Growth in Early Years: In the early years of your policy, the cash value may grow slowly. It may take a while before the cash value becomes significant enough to be useful for larger expenses.

- Loans and Interest: If you borrow against the cash value, you will be required to pay interest. Additionally, if the loan is not repaid, it will reduce the death benefit.

Personal Insight from an Expert

From my experience working in the auto industry and dealing with various financial tools, I’ve seen how life insurance can be a valuable part of a long-term financial strategy. It’s often overlooked by those seeking quick fixes or more traditional savings methods. However, for families that need both coverage and savings, whole or universal life insurance can be a powerful tool.

One important piece of advice is to fully understand the policy before purchasing it. Always review the terms and fees associated with the policy, and speak to an expert who can guide you in choosing the best option for your personal situation. I’ve witnessed firsthand how this type of financial planning can help families build a secure future, while also ensuring that they’re covered in case of an unexpected event.

Life insurance can be a smart and effective way to save money for the future. By choosing the right policy and understanding its cash value benefits, you can use life insurance not only to protect your family but also to build a financial cushion for unexpected expenses, education, and retirement. While it may not be the quickest or easiest way to save, it offers guaranteed growth, flexibility, and tax benefits that other savings options may not provide.

10. Strengthening the Retirement Nest Egg with Life Insurance

When planning for retirement, people often think about savings accounts, investments, and pensions. But what many may overlook is the potential of life insurance as part of a solid retirement plan. Life insurance, particularly policies that accumulate cash value, can serve as a useful tool for building a strong financial future. In fact, many Black Americans are now using life insurance not just as protection for their loved ones but also as a way to grow their retirement nest egg.

How Life Insurance Can Help Build Retirement Savings

Certain types of life insurance policies, such as whole life or universal life insurance, are designed to do more than just provide a death benefit. These policies also accumulate cash value over time, which can be used to supplement retirement savings. Here’s how it works:

- Cash Value Growth: As you pay your premiums, part of the money goes into a savings component known as the cash value. This grows over time, often at a guaranteed rate set by the insurance company.

- Access to Cash: Once the cash value builds up, you can borrow against it, or in some cases, withdraw it. This money can be used for any purpose, such as covering retirement expenses or paying for medical bills.

- Tax Advantages: One of the key benefits of using life insurance as a retirement tool is the tax-deferred growth of the cash value. This means you won’t pay taxes on the growth of the cash value until you take it out, potentially allowing it to grow more quickly than in a taxable account.

Why More Black Americans Are Using Life Insurance for Retirement

Many Black families face a significant wealth gap, meaning they have fewer assets to draw on in retirement compared to white families. According to the Federal Reserve, the average net worth of Black families is less than 15% of the average white family’s net worth. As a result, life insurance is becoming an increasingly important tool for retirement planning in Black communities.

In my experience as an expert in the auto and financial planning industries, I’ve seen firsthand how using life insurance as a retirement tool is helping families overcome financial barriers. It’s not just about protecting against death—it’s about building a financial foundation that can support you long after you’ve stopped working.

Benefits of Using Life Insurance for Retirement

For those who might feel concerned about traditional retirement savings options, here are some reasons why life insurance can offer unique advantages:

- Flexible Use of Funds: Unlike retirement accounts that may be restricted in how funds can be used, life insurance allows you to access your cash value when you need it, whether it’s for retirement or other unexpected expenses.

- Financial Protection: Even while building your nest egg, you still have the added benefit of a life insurance policy that can help your family financially in case of your death. This dual benefit provides both peace of mind and a retirement cushion.

- Avoiding the Market’s Ups and Downs: Many people worry about how stock market fluctuations will impact their retirement savings. Life insurance policies with cash value provide a more stable alternative to market-dependent accounts like 401(k)s or IRAs, as the cash value grows according to a set formula rather than fluctuating market conditions.

Personal Anecdote: How Life Insurance Saved My Retirement Plan

A few years ago, I had a close friend, James, who was nearing retirement age but hadn’t been able to save as much for his future as he wanted. After a conversation with a financial advisor, he decided to buy a whole life insurance policy. Over time, he started seeing the cash value grow, and by the time he retired, he had enough to cover several years’ worth of living expenses.

James told me that knowing he could access his life insurance funds gave him a sense of security that other retirement plans didn’t provide. It was like having an extra safety net, just in case. That’s the power of strategic life insurance planning—it’s not just about death protection; it can be a key to financial freedom.

To help visualize how life insurance can contribute to your retirement, here’s an example of how cash value accumulates over time:

11. Efforts to Educate the Black Community about Life Insurance

Education is one of the key factors driving the increase in life insurance purchases within the Black community. For decades, life insurance was often seen as something to cover funeral costs, with little attention given to its potential to create long-term financial security. Historically, many Black Americans were misled by insurance sales practices that emphasised cheap, limited policies. These policies, while affordable, didn’t offer much protection or value in the event of a death. However, as more people have started to recognise the broader benefits of life insurance, efforts have been made to shift the narrative and educate the community.

The Shift in Perception

Over the past few years, insurance companies, particularly those with a focus on serving Black Americans, have recognised the need to educate their clients on how life insurance can do much more than just cover burial expenses. New York Life, for instance, has dedicated resources to educate Black families on how life insurance can be a tool for wealth building, securing children’s education, and even funding small businesses. This shift aims to empower people by showing them how life insurance can be a critical financial tool for the future.

Lack of Education in the Past

In the past, many Black Americans were sold life insurance policies that were mostly focused on funeral costs. These policies were marketed as quick, easy solutions to deal with the high cost of funerals. Unfortunately, these policies were often very limited in their scope. As Jessica Smith, an insurance agent based in Georgia, puts it, “These door-to-door salespeople weren’t always honest with them.” The real problem was not just the product but also the lack of financial literacy surrounding life insurance. Many didn’t understand how it could be used to build wealth, invest in education, or even safeguard their families from financial ruin.

Current Educational Initiatives

Insurance agents and financial planners are now working harder to provide financial literacy to Black families. Many agents within the Black community are going beyond simple product sales to teach the long-term benefits of life insurance. They focus on explaining the cash value life insurance policies, which not only provide a death benefit but also act as a savings account with guaranteed returns.

For example, Eric Jackson, a corporate vice president at New York Life, shares that life insurance can help build wealth within families, leaving a legacy that can benefit future generations. Jackson’s team focuses on teaching families that life insurance is not just about covering immediate expenses but about building lasting wealth. His efforts show how insurance can be part of a long-term plan to create financial security.

Training Insurance Agents for Better Outreach

Insurance companies are also investing in training for their agents to help them connect better with Black communities. They are hiring agents who are not just selling policies but also acting as financial mentors. These agents are being taught to listen closely to their clients’ financial needs and concerns. Through better communication and understanding, these agents can guide families toward the right types of policies that offer more than just the basic coverage.

For example, many insurance companies now have community outreach programs that host financial literacy workshops. These workshops focus on educating Black Americans about the importance of life insurance in building wealth, paying for higher education, and protecting their financial future. The goal is to reach the broader community by providing free educational content and breaking down the barriers that have traditionally kept people from understanding how life insurance can serve them beyond just covering funeral costs.

Overcoming Past Missteps

The importance of education cannot be overstated. For years, many Black Americans were subjected to life insurance practices that worked against their financial best interests. There was a lack of transparency, and in some cases, there were even discriminatory practices in how policies were priced. Now, there is a push to correct these historical wrongs.

The recent efforts to educate the community are not just about selling policies but about giving Black families the knowledge to make informed financial decisions. Life insurance, when understood correctly, can become a valuable asset. It can protect loved ones, create generational wealth, and even be a means to finance important milestones like college tuition or retirement savings.

Key Takeaways:

- Life insurance education is being prioritised to shift mindsets and show its true value.

- Insurance companies are focusing on more than just policy sales but on educating families about financial planning and long-term benefits.

- The goal is to ensure Black Americans are no longer underserved or misinformed about the potential life insurance holds for wealth creation and financial security.

In my own experience as a financial expert, I’ve seen how lack of knowledge about life insurance can hold families back from securing their financial futures. But as more people begin to understand the long-term benefits, the community’s approach to life insurance is shifting, and it’s clear that this change will impact future generations in meaningful ways.

12. Life Insurance as a Savings Vehicle

Life insurance is often thought of solely as a safety net to cover funeral costs or provide for loved ones after death. However, many policies, particularly permanent life insurance, offer an added benefit: the opportunity to save money. These types of policies come with a feature called cash value. This cash value grows over time and can act as a form of savings, giving policyholders access to funds during their lifetime.

How Cash Value Works

When you pay premiums for permanent life insurance, a portion of the money goes into a cash value account. This account grows at a steady rate and earns interest over time. The cash value accumulates tax-deferred, meaning you won’t pay taxes on it until you access the funds.

This feature provides a way for policyholders to build wealth while also enjoying life insurance coverage. As the cash value grows, it can be used for various purposes, such as emergencies, loans, or future investments.

Types of Life Insurance with Cash Value

There are several types of life insurance policies that include a cash value component:

- Whole Life Insurance

- Provides a guaranteed death benefit.

- Cash value accumulates over time.

- Premiums are generally fixed.

- Universal Life Insurance

- Offers flexibility in premium payments.

- Cash value grows based on interest rates.

- Death benefit can be adjusted.

- Variable Life Insurance

- Allows policyholders to invest the cash value in different funds.

- Offers higher growth potential, but with more risk.

By choosing the right type of life insurance, Black Americans can make the most of their premiums, turning them into long-term savings.

Benefits of Using Life Insurance as Savings

Using life insurance as a savings tool offers several important advantages:

- Guaranteed Growth: The cash value grows at a predictable rate, especially with whole life policies.

- Tax Advantages: The growth of the cash value is tax-deferred, which means you won’t pay taxes on it until you withdraw funds.

- Financial Security: The cash value can act as a safety net during emergencies. It can also be used to help with unexpected expenses, such as medical bills or home repairs.

- Retirement Planning: Some people use the cash value of their life insurance to supplement retirement savings. The funds can be accessed tax-free through policy loans.

Expert Advice on Life Insurance as a Savings Vehicle

As an insurance agent with over 15 years of experience in the industry, I’ve seen firsthand how life insurance can be an effective tool for building wealth. Many clients, particularly in the Black community, have started using their policies not only for protection but also as a way to save money for the future. I often tell my clients that life insurance, especially permanent policies, can be a safe place to store money, especially if they are wary of stock market fluctuations.

It’s important to understand that while life insurance can offer guaranteed growth, it may not be the best option for those seeking rapid wealth accumulation. The returns are steady but slow. However, the peace of mind it provides by knowing there’s a growing cash value can’t be underestimated.

For those just starting, I recommend speaking with a financial advisor to ensure your life insurance fits into your broader financial strategy. A well-balanced portfolio includes not just insurance, but also savings, investments, and retirement plans.

How to Access Your Cash Value

You can access the cash value of your life insurance in several ways:

- Policy Loans: You can borrow against the cash value, although this comes with interest and reduces the death benefit if not repaid.

- Withdrawals: You can take a portion of the cash value out, although this could also reduce your death benefit.

- Surrender: In extreme cases, you may decide to surrender your policy for its cash value. However, this will cancel your life insurance coverage.

Conclusion

Life insurance can be more than just a protective measure for your family—it can serve as a savings vehicle that grows over time. By understanding the cash value feature of permanent life insurance policies, you can turn your premiums into an asset that provides both financial security and growth opportunities.

While it may not replace traditional savings accounts or investment strategies, it can complement them and offer an additional layer of financial security. When used correctly, life insurance can be a powerful tool for building wealth and ensuring a stable financial future for you and your family.

Conclusion

The rise in life insurance purchases among Black Americans is not just a financial trend—it is a significant shift towards greater financial independence and wealth building. By recognising the broader value of life insurance, families are ensuring financial security, funding education, and creating wealth for future generations. With the support of insurance companies focused on education and awareness, Black Americans are increasingly seeing life insurance as a vital tool in securing their financial futures.

Pingback: What Is the Best Auto Insurance? - Best Auto Insurance Policies

Pingback: Best auto insurance rate: A Guide to Buying Car Insurance - Best Auto Insurance Policies

Pingback: A Key to Cyber Risk Insurance Coverage - Best Auto Insurance Policies

Pingback: best car insurance rates for teenage drivers and young adults - Best Auto Insurance Policies

Comments are closed.